Featured

Table of Contents

Reuse needs attribution under CC BY 4.0. Required More Information on Market Gamers and Rivals? Download PDF January 2026: Salesforce concurred to acquire Own Business for USD 1.9 billion to bolster multi-cloud backup and compliance abilities. December 2025: Microsoft launched Copilot for Dynamics 365 Finance, reporting 40% quicker month-end close cycles among early adopters.

INTRODUCTION1.1 Study Assumptions and Market Definition1.2 Scope of the Study2. MARKET LANDSCAPE4.1 Market Overview4.2 Market Drivers4.2.1 AI-Powered Workflow Automation Adoption4.2.2 Shift to Subscription, SaaS Income Models4.2.3 Demand for Unified Data Fabrics4.2.4 Low-Code, No-Code Platforms in Citizen Development4.2.5 Emerging Vertical-Specific Copilots4.2.6 Algorithmic ESG Expense Optimizers4.3 Market Restraints4.3.1 Escalating Cloud Spend Optimisation Pressure4.3.2 Growing Open-Source Alternatives4.3.3 Data-Sovereignty and Cross-Border Compliance Hurdles4.3.4 Scarcity of Prompt-Engineering Talent4.4 Industry Value Chain Analysis4.5 Regulatory Landscape4.6 Technological Outlook4.7 Porter's 5 Forces Analysis4.7.1 Bargaining Power of Suppliers4.7.2 Bargaining Power of Buyers4.7.3 Risk of New Entrants4.7.4 Hazard of Substitutes4.7.5 Intensity of Competitive Rivalry4.8 Impact of Macroeconomic Aspects on the Market5.

COMPETITIVE LANDSCAPE6.1 Market Concentration6.2 Strategic Moves6.3 Market Share Analysis6.4 Company Profiles (includes Worldwide Level Overview, Market Level Summary, Core Segments, Financials as Available, Strategic Details, Market Rank/Share for Secret Companies, Services And Products, and Recent Advancements)6.4.1 Microsoft Corporation6.4.2 IBM Corporation6.4.3 Oracle Corporation6.4.4 SAP SE6.4.5 Snowflake Inc. 6.4.6 Salesforce Inc. 6.4.7 Adobe Inc.

6.4.9 Sage Group plc6.4.10 Workday Inc. 6.4.11 ServiceNow Inc. 6.4.12 Epicor Software Corporation6.4.13 Infor6.4.14 Oracle NetSuite6.4.15 monday.com6.4.16 Deltek Inc. 6.4.17 Zoho Corporation6.4.18 Atlassian Corporation6.4.19 Freshworks Inc. 6.4.20 HubSpot Inc. 6.4.21 Odoo S.A. 7. MARKET CHANCES AND FUTURE OUTLOOK7.1 White-Space and Unmet-Need Assessment You Can Purchase Components Of This Report. Examine Out Prices For Particular SectionsGet Rate Separation Now Service software application is software that is used for service functions.

The Business Software Market Report is Segmented by Software Application Type (ERP, CRM, Organization Intelligence and Analytics, Supply Chain Management, Personnel Management, Finance and Accounting, Project and Portfolio Management, Other Software Types), Deployment (Cloud, On-Premise), End-User Market (BFSI, Healthcare and Life Sciences, Government and Public Sector, Retail and E-Commerce, Transport and Logistics, Manufacturing, Telecom and Media, Other End-User Industries), Organization Size (Large Enterprises, Small and Medium Enterprises), and Geography (The United States And Canada, South America, Europe, Asia Pacific, Middle East, Africa).

AI vs. Manual Workflows: Which Succeeds?

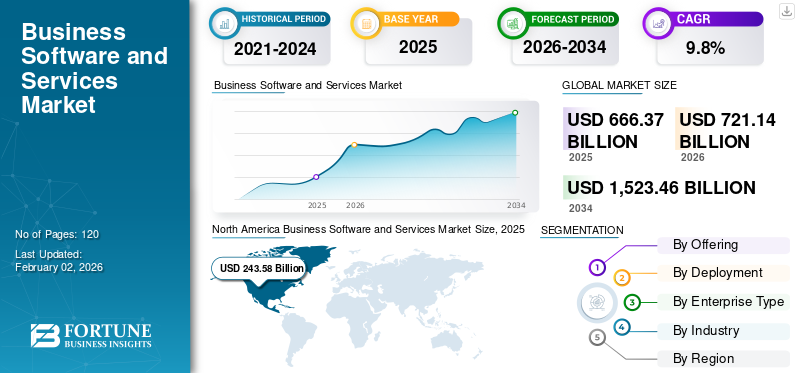

Low-code platforms lead development with a projected 12.01% CAGR as organizations widen citizen advancement. Interoperability requireds and AI-driven clinical workflows push healthcare software application costs upward at a 13.18% CAGR.North America maintains 36.92% share thanks to thick cloud facilities and a mature client base. The leading 5 suppliers hold roughly 35% of revenue, indicating moderate fragmentation that favors niche specialists in addition to platform giants.

Software application spend will speed up to a spectacular 15.2% in 2026 per Gartner. It will stay the largest and fastest-growing section of the $6 Trillion business IT spent. A massive number with record growth the biggest development rate in the entire IT market. But before you begin commemorating, here's what's really occurring with that cash.

CIOs are bracing for the impact, setting 9% of the IT budget plan aside for rate boosts on existing services. 9 percent of every IT budget in 2025-2026 is being assigned just to pay more for the exact same software business currently have. While spending plans for CIOs are increasing, a significant portion will simply offset cost boosts within their persistent costs, implying nominal spending versus real IT spending will be skewed, with rate walkings soaking up some or all of spending plan growth.

Why Should Marketing Automation Scale?

Out of that sensational 15.2% growth in software spending, approximately 9% is just inflation. That leaves about 6% for actual new spending.

Next year, we're going to invest more on software with Gen AI in it than software application without it, and that's just 4 years after it became readily available. This is the fastest adoption curve in business software history. In 2024, enterprises attempted to construct their own AI.

They worked with ML engineers. They try out custom models. Many of it failed. Expectations for GenAI's abilities are decreasing due to high failure rates in preliminary proof-of-concept work and frustration with existing GenAI outcomes. Now they're done building. Ambitious internal jobs from 2024 will deal with examination in 2025, as CIOs go with commercial off-the-shelf solutions for more foreseeable execution and business value.

How to Preserve Market Share Utilizing High

This is the most important shift in the whole projection. Enterprises offered up on build. They're going all-in on buy. Enterprises purchase the majority of their generative AI abilities through vendors. You don't require a customized AI option. You don't need to use POCs. You need to deliver AI functions into your existing item that produce enormous ROI.

Even Figma still isn't charging for much of its brand-new AI functionality. It's not recording any of the IT budget plan growth that method. Despite being in the trough of disillusionment in 2026, GenAI features are now ubiquitous throughout software application currently owned and run by business and these functions cost more money.

Reviewing B2B Scaling Frameworks

Everybody understands AI isn't magic. Due to the fact that at this point, NOT having AI functions makes your product feel out-of-date. The cost of software application is going up and both the expense of functions and functionality is going up as well thanks to GenAI.

Considering that 9% of spending plan growth is consumed by price increases and most of the rest goes to AI, where's the money actually coming from? 37% of finance leaders have actually already paused some capital costs in 2025, yet AI financial investments remain a leading concern.

54% of infrastructure and operations leaders said expense optimization is their leading goal for embracing AI, with lack of spending plan mentioned as a top adoption challenge by 50% of participants. Business are cutting low-ROI software to fund AI software.

CIOs expect an 8.9% cost boost, on average, for IT products and services. Include AI functions and you can justify 15-25% cost boosts on top of that base inflation. GenAI functions are now common across software currently owned and run by business and these features cost more money.

Maximizing Value through Smart Enablement

Right now, purchasers accept "we added AI functions" as justification for rate increases. In 18-24 months, AI will be so standard that it won't validate superior rates any longer. Ship AI features into your core item that are necessary enough to monetize Announce price boosts of 12-20% connected to the AI abilities Position the increase as "AI-enhanced functionality" not "price boost" Show some cost optimization or performance gains if possible Companies that execute this in the next 6 months will capture prices power.

{kind=link}

Latest Posts

Supporting Account Teams with Actionable Customer Intelligence

Strategic Methods for Scaling Digital Impact

Maximizing Scalability with Microservices Integration